the efficiency of Medicare vs. private insurance

Some back-and-forth recently on the Health Affairs blog about the efficiency of Medicare vs. private insurance:

followed by

Archer yesterday

Archer talks past Goodman and finds more studies which ignore the points he's making. And of course, she fails to note that private insurance is made far less efficient by all sorts of government intrusion in the market-- most notably, the vast subsidies to purchase health insurance, but also mandates on insurers/insurees and restrictions in competition between insurers.So, we're comparing a private insurance market, bound and beaten by the govt, to whatever the govt does. Not exactly a fair fight, if one is trying to compare "markets" to govt provision.

Archer talks past Goodman and finds more studies which ignore the points he's making. And of course, she fails to note that private insurance is made far less efficient by all sorts of government intrusion in the market-- most notably, the vast subsidies to purchase health insurance, but also mandates on insurers/insurees and restrictions in competition between insurers.So, we're comparing a private insurance market, bound and beaten by the govt, to whatever the govt does. Not exactly a fair fight, if one is trying to compare "markets" to govt provision.

I'm not sure whether Goodman will find it worthwhile to respond to this. Stay tuned...

Highlights from Goodman and Saving:

...most seniors would like to keep Medicare just like it is. A similar view is held by a small, but vocal group on the left that favors single-payer national health insurance. The Physicians for a National Health Program, for example, claims that Medicare has lower administrative costs than private insurance and is able to use its monopsony (single-buyer) power to suppress provider fees...

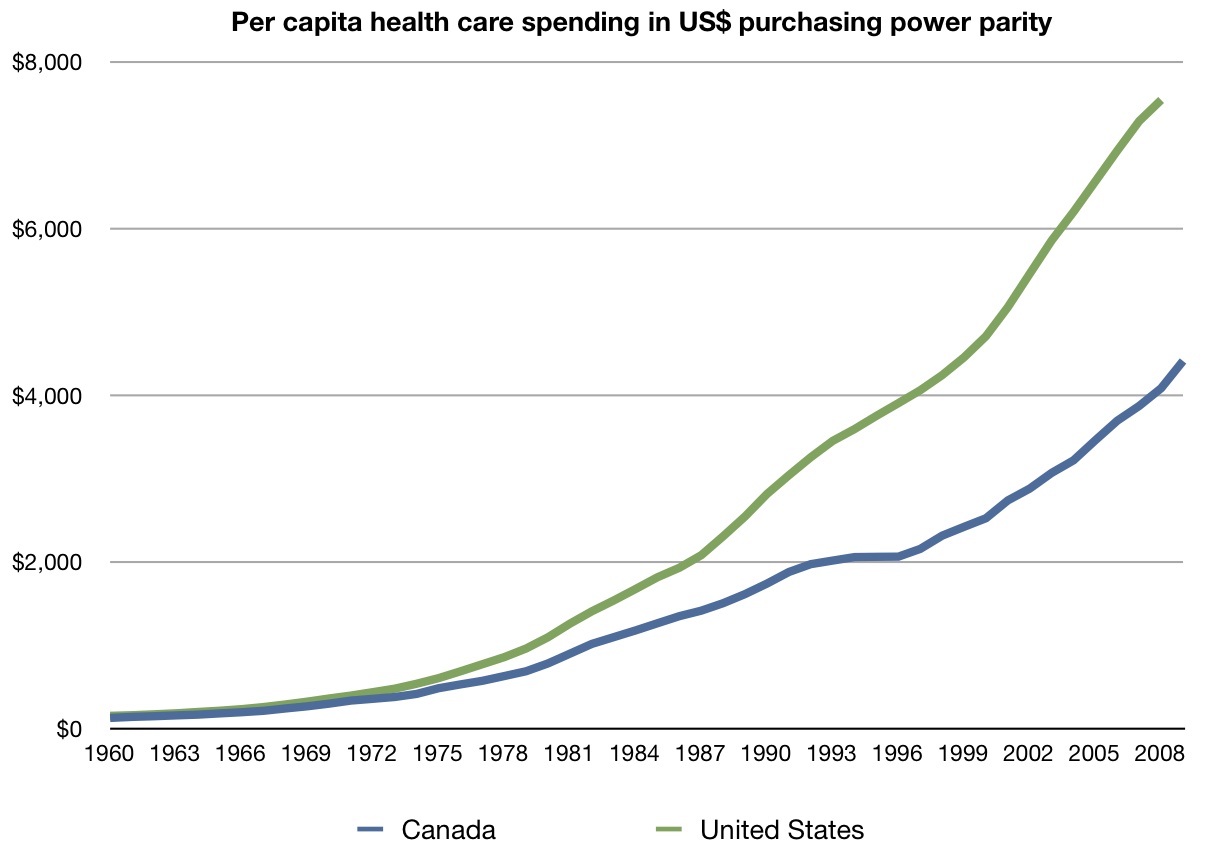

Paul Krugman, writing in The New York Times, also argues this way. He points to a chart (see Figure I) which seems to show that Medicare per capita spending is growing at a slower rate than private insurance. Krugman, along with others, touts the slower rate growth in the Canadian health care system...

Let’s begin with a fundamental point that almost everyone tends to ignore. Medicare is not actually managed by the federal government. In most places it is managed by private contractors, including such entities as Cigna and Blue Cross...

What about the claim that Medicare’s administrative costs are only 2%, compared to 10-15% for private insurers? The problem with this comparison is that it includes the cost of marketing and selling insurance as well as the costs of collecting premiums on the private side, but ignores the cost of collecting taxes on the public side. It also ignores the substantial administrative cost that Medicare shifts to the providers of care.

Studies by Milliman and others show that when all costs are included, Medicare costs more, not less, to administer. Further, raw numbers show that, using Medicare’s own accounting, its administrative expenses per enrollee are higher than private insurance. They are lower only when expressed as a percentage – but that may be because the average medical expense for a senior is so much higher than the expense for non-seniors...

Ironically, many observers think Medicare spends too little on administration, which is one reason for an estimated Medicare fraud loss of one out of every ten dollars of Medicare benefits paid. Private insurers devote more resources to fraud prevention and find it profitable to do so.

The Argument Based On Government Single-Buyer Market Power: Five Problems

Health care markets are local. First, we don’t buy health care in a national market. We buy locally. And in local markets, private entities are often as big, or bigger, than Medicare (the auto companies in Detroit, for example, or the mine workers and their employers in West Virginia). There is nothing the US government can do that a lot of private companies and unions cannot also do...nothing is stopping the auto companies and the UAW from creating a global budget and rationing care for auto workers just the way the Canadians do it. That they choose not to do so is telling. Side effects of suppressing provider fees. Second, there are negative consequences from unduly suppressing provider fees. Doctors can leave...The effects of price controls in health care will be similar to their effects in other markets.

Cost-shifting. Third, the suppression of provider payments shifts costs from patients and taxpayers to providers. Shifting costs, however, is not the same thing as controlling costs...

Political pressures and lobbying. Fourth, the argument overlooks the fact that public insurance in a democracy is ultimately subject to pressures at the ballot box....

posted by Eric Schansberg @ 9:15 AM

2 Comments

![]()

![]()

{kind=link}

2 Comments:

This is good stuff - thanks for posting.

The idea of the government using its power to suppress costs is a noble one and is perhaps the first time it has appeared to me as such.

The problem with this noble idea is that it is only treating the symptoms and not the causes.

What I am suggesting is that there needs to be a mechanism by which consumers have the ability to push back on providers in terms of cost and quality. In other words, if I go to the doctor for a procedure and the doctor fails to improve my condition or even makes it worse, I cannot go back to the doctor and demand my money back. I can either pay him/her MORE money to try again or I can go to another doctor. Where else in life does this happen?

We need to stop treating doctors as all-knowing beings and start holding them accountable for not only their performance, but what they are charging.

How do we start the process for getting health insurance extricated from the realm of employers and into the realm of insurance brokers? This seems like a logical first step in producing real improvements. More competition and less gov't beauracracy will manage costs.

Usually, markets do a nice job of allowing "push back", between demand's preference for more quality and quantity at lower prices, and supply's preference for higher profits.

In the case of health care/insurance, that has been boggled by vast subsidies and many regulations. In most markets, consumers and suppliers are generally happy, usually engaging in mutually beneficial trade. But in health care (and other govt-run or heavily-govt-influenced realms), people on all sides of trade get routinely bent.

To an economist, the best answer is to tax fringe benefits (lowering the marginal tax rate on all forms of compensation to keep it revenue-neutral). This would eliminate the subsidy. Unfortunately, this would be politically difficult, given a public that doesn't pay much attention and policy makers who are limited in terms of courage and imagination. Next best is Health Savings Accounts and watch us continue to limp toward true insurance (covering rare, catastrophic events), with high deductibles.

Post a Comment

Subscribe to Post Comments [Atom]

<< Home